Charitable Giving using Life Insurance

Article Licenses: DL, unknown, unknown

Advisor Licenses:

Compliant content provided by Adviceon® Media for educational purposes only.

Generosity is for everyone. All it takes is a willing spirit and the courage to be used for something greater than ourselves. 1

Generosity is for everyone. All it takes is a willing spirit and the courage to be used for something greater than ourselves. 1

Permanent life insurance is a cost-effective way to make a much more significant contribution to the charity of your choice than would otherwise have been possible. Gifting a new policy or an existing policy can help the charity of your choice. Determine what charity aligns with your life purpose and will bring you the most satisfaction.

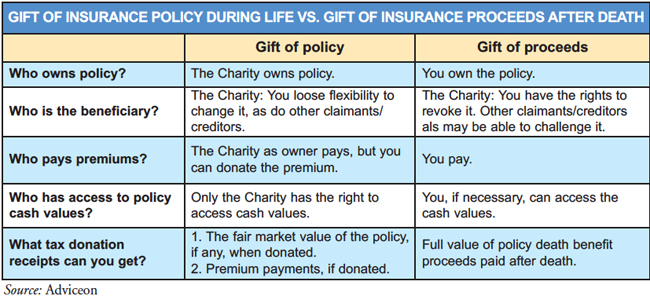

There are two effective methods to achieve this. One is an outright gift of a life insurance policy, making the charity the policy owner. The second is gifting the death benefit proceeds while you retain ownership.

1. Making the charity the owner of a life insurance policy

This strategy also side-steps some potential problems if such a legacy is made via your estate.

- You purchase a policy on your life, making the charity the owner and beneficiary.

- Only the charity can change the beneficiary.

- The charity as the established owner of the policy mitigates any dispute over ownership by other heirs once you die.

- You make donations to the charity that then pays the premiums.

- You can receive a tax break for the premiums you’ve paid via the charity.

- The charity receives all of the death benefit proceeds when you die free of tax.

- The benefit payout cannot be contested, taxed, or claimed by your creditors.

- The capital death benefit guarantees payout to the charity, and in some cases, the death benefit may grow over time. The death benefit is paid tax-free to the charity of your choice.

The tax benefits while you are alive When the charity owns the policy, under Canadian tax legislation, you can receive a tax break for the premiums that you’ve paid during your lifetime, insofar as they are made after the charity owns the policy. In addition, you can receive a tax receipt for the fair market value of any cash value of the policy when you donate an existing policy. There are no further tax deductions in your estate (on your last tax return done by your executor after your death).

2. You own the life insurance policy

In this strategy, you own a life insurance policy on your life, while the charity receives the full proceeds of the policy upon your death.

- You own the policy.

- You have access to any cash value of the policy, if necessary.

- The charity is the beneficiary though you can change it.

- Other claimants, such as a creditor, may challenge the right to the proceeds.

- Tax benefits to the estate (your final tax return) may apply for some of the policy proceeds after your death. Note: Discuss with your tax advisor.

As the policy owner, you can change beneficiaries and have full access to any accrued cash value over your lifetime. The proceeds from the death benefit are not subject to probate nor estate administration fees, nor will the gift be on the public record.

When a charity is the designated beneficiary of a life insurance policy on your life, the charity receives the proceeds of the death benefit upon your death. Your tax advisor can advise you if the tax-free benefit paid to the charity, as the beneficiary, generates any disposition to your estate (as it would on an owned asset such as a gifted cottage that has accrued value over time).

The tax benefits to your estate after your death The charity will issue a charitable receipt for the entire amount paid to them in the year of your death. The entire capital created at your death, referred to as the death benefit, will account for a charitable donation on your final tax return prepared by your executor.

Note: Your tax advisor can assess any tax due in the estate for cash values accrued according to changing tax law.

Life insurance can be part of an ongoing charitable gift plan or offer your estate a significant tax break when the death benefit pays out to the charity.

David Toycen sums up the importance of our gifts to charity: If I am generous to someone, that person will likely be generous to someone else. There is an argument to be made that the universe was created to operate this way. 2

Ask your life insurance or tax advisor to guide you in strategically setting up a charitable life insurance policy to enable the best possible tax savings.

1, 2 The Power of Generosity, Dave Toycen. Pres. World Vision, Canada, (Harper Collins Publishers, 2004)

The Advisor and Manulife Securities Incorporated, ("Manulife Securities") do not make

any representation that the information in any linked site is accurate and

will not accept any responsibility or liability for any inaccuracies in

the information not maintained by them, such as linked sites. Any opinion

or advice expressed in a linked site should not be construed as the opinion

or advice of the advisor or Manulife Securities. The information in this

communication is subject to change without notice.

This publication contains opinions of the writer and may not reflect opinions

of the Advisor and Manulife Securities Incorporated, the information contained

herein was obtained from sources believed to be reliable, no representation,

or warranty, express or implied, is made by the writer, Manulife Securities or

any other person as to its accuracy, completeness or correctness. This

publication is not an offer to sell or a solicitation of an offer to buy any

of the securities. The securities discussed in this publication may not be

eligible for sale in some jurisdictions. If you are not a Canadian resident,

this report should not have been delivered to you. This publication is not

meant to provide legal or account advice. As each situation is different you

should consult your own professional Advisors for advice based on your

specific circumstances.